Photo courtesy of APO Bookkeeping

Reconciling all your accounts on a monthly basis is the single most important thing you could do for yourself and your business. There are numerous software available to help make this process effortless, but regardless of the software or lack thereof, monthly reconciliations must be done in order to avoid costly mistakes.

Why reconciling your accounts is so important

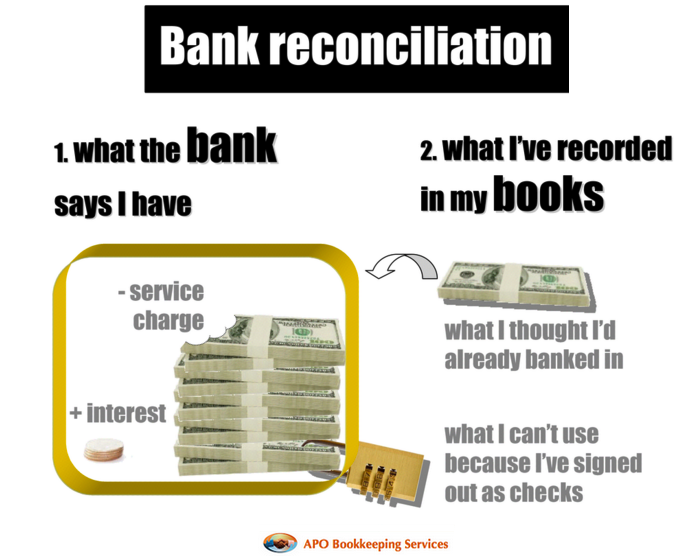

Reconciliation is so important because it is the only way to be certain your account balances are in agreement with your financial institutions, vendors, etc. Reconciling your accounts ensures that the actual monies spent matches the monies leaving an account at the end of a period, and that the actual monies put in also matches the monies coming into an account at the end of a period. When you reconcile your bank statement every month with your QuickBooks balance for example, you will become aware of checks that have not been cleared, and this will help you track down any potential missing payments. You will also become aware of any deposits you have made that are not showing up. This is rare, but it does happen! In addition, you can use your reconciliation statement to make sure your other company transactions are going through and have been calculated for the proper amounts.

There are aspects of your financials that reconciliation will not take care of such as personal monies you used up for the business, but have not recorded, as well as other assets and liabilities that may not have affected your reconciliations. So, reconciliations alone will not make your “books” accurate. You may need the help of a bookkeeper and CPA to get these aspects worked out; bookkeeper to ensure everything is recorded, and the CPA to analyze what is recorded and make the final call on whether the entries make the final books better or worse for the business.

It is imperative that controls – checks and balances, are in place to monitor the business banking and credit card transactions. For large firms you should have multiple hands assigned to cross-checking banking activities on a regular basis. For small businesses, you the owner should check your banking transactions – at least on a monthly basis to ensure everything is on par – even though you may have someone assigned to reconcile your accounts. When bank statements are not monitored and reconciled, the potential for undetected loss is high. Not all employees or accounting firms are honest, and you may not miss money that has been taken for some time. This is the reason some employees are able to embezzle hundreds if not thousands of dollars over time. Reconciling your bank statement helps you prevent losses and may indicate a potential problem in your accounting system.

What accounts can be reconciled and how to reconcile them

Any account that you get a statement for, showing a beginning and ending balance, can and should be reconciled. This includes: bank accounts, credit card accounts, loans and lines of credit accounts, and vendor accounts. There is also the internal reconciliation of many accounts, including customer receivables accounts.

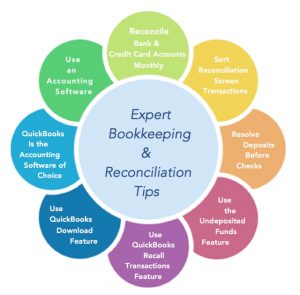

Reconciling any account in software such as QuickBooks is a moderately easy feat. The time it takes to reconcile your accounts will depend on the accuracy of the transactions entered in your accounting system; if they were entered correctly – precise numbers and debit/credit accounted, your reconciliation should be done in a shorter time. If however they were not carefully entered, it may take you a longer period of time trying to locate the discrepancies. If this is the case, you may need to go transaction by transaction verifying your bank statement numbers with QuickBooks and marking each cleared as you go along. This can be tedious if there are many transactions; however, it must be done. You can see why it is vital to enter all transactions accurately to begin with. If you are using QuickBooks or other similar software, you should take advantage of the “download” feature. Initially, you will need to edit and select the right accounts as well as input the vendor or customer before you add or match each transaction; however, QuickBooks will begin to recognize each transactions that you have edited after a while and most importantly your numbers will be accurate with the correct corresponding debit or credit.

Using the ask my accountant account for questionable transactions

QuickBooks has a “Ask My Accountant” option in their chart of accounts that can be a huge ally in helping you reconcile. At times you may have transactions that you are not sure how to enter, or how to enter to be beneficial to your business. Any questionable transactions should be coded to “Ask My Accountant” so that you can continue with your reconciliations while having a conspicuous account to house them and have them easily accessed and rectified at a later date by your CPA.

So, reconcile your accounts on a monthly basis! You want to ensure that all the transactions are in your ledger and accurately accounted for. It is easy to forget to enter an expense or a payment when you are in a rush or if you have misplaced a receipt, so cross-checking against the account statement can be a good safety net for your own books. Doing so will ensure that you are getting paid—and paying people back—promptly, which in turn will help you keep other parts of your accounting in order such as your cash flow, profit and loss statement, etc. Of course you can trust your suppliers and creditors to charge appropriately, but everyone makes mistakes and are prone to err.

How to Reconcile Your Monthly Bank Statements With Your Bank Balance in QuickBooks

How to Reconcile Your Monthly Bank Statements With Your Bank Balance in QuickBooks

How to Reconcile Your Paypal Account With QuickBooks

I haven’t learned the reconciliation process as yet, and even though my bookkeeper is handling it, I want to have the basic knowledge of how it is done. I like to know how things are done in all aspects of my business. I also want to implement it for my personal use, which I will be compiling myself on QuickBooks Online.

This will surely help me, thanks to you Eugénie! Bookmarked!

HI Janice, happy you are taking the initiative to learn a bit about the various aspect of your business. It could only help! I’m sure you will master the recon process. Good luck with your personal updates!